“Sometimes when you try to pour tomato ketchup onto your plate, nothing comes out. Then you leave it for a few minutes, and the whole bottle glubs out over everything.”

Scoop: Sir Lucian Grainge doesn’t use squeezy condiments at the dinner table. More searing music business insights from MBW when we have them.

Believe it or not, Grainge’s aside about ketchup on UMG’s Q1 earnings call last Wednesday (April 29) amplified an astute – and gently cutting – point to listening analysts.

In essence: UMG is a business built on human creativity, and no matter how much investors might like us to whip those humans to make them more productive/predictable, it ain’t gonna work. The good news? Universal’s sprawling roster and catalog guarantees that, more quarters than not, a viscous flow of revenues… well, glubs out over everything.

Grainge reached for the ketchup analogy to frame a quarter in which UMG showed unspectacular yet solid growth in both revenue and EBITDA, but a slight YoY downturn in market share.

That downturn was pinned on “a light release schedule” in the quarter – aka the seasonality of superstar frontline releases. It had nothing to do with dilution from a deluge of AI music, confirmed Universal digital boss, Michael Nash.

“Keep in mind that last year, as the flood of AI content was rising to the point of tens of thousands of tracks [per day], we had our highest recorded music market share since 2013 according to Music & Copyright,” said Nash. “That’s empirical disproof of the idea that a [UMG] market share issue is tied to AI dilution.”

Here’s what else caught my attention from UMG’s earnings…

1) Artists are about to get paid a nine-figure sum from UMG’s Spotify stock sale. Analysts call that ‘leakage’. How respectful…

Universal used its latest earnings to announce that it’s selling 50% of its holding in Spotify.

The company plans to deploy its proceeds from this sale towards a EUR €1 billion stock buyback program, taking advantage of a depressed share price.

Spotify’s own share price had a bumpy week, of course, plunging double-digits after its Q1 earnings call last Tuesday (April 28).

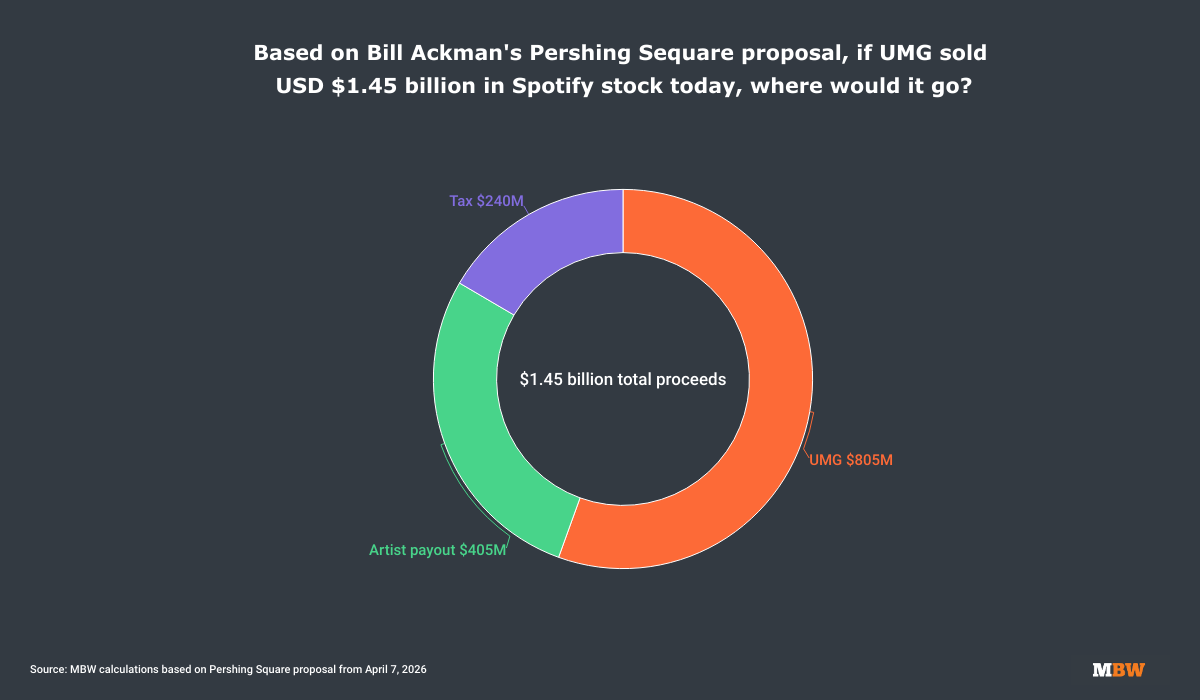

As a result, UMG’s ~3.10% stake in SPOT is currently worth approximately USD $2.9 billion, of which 50% would be worth $1.45 billion.

UMG has confirmed that it will distribute a portion of the proceeds from this $1.45 billion windfall to artists, and has previously committed to overlook/ignore unrecouped balances when it does so.

On UMG’s Q1 earnings call, BofA Securities analyst, Adrien de Saint Hilaire, asked: “Regarding the Spotify stake, if you were to sell it at the current share price, how much leakage would there be in terms of tax and proceeds to artists?”

Ah, leakage.

A word most commonly associated with soggy plumbing and urinary incontinence.

And also now, apparently, artists – for the inelegant act of absorbing a few dollars from a Spotify market cap built entirely on their labor.

Won’t someone please pass the TENA Lady?

“A word most commonly associated with soggy plumbing and urinary incontinence. And also now, apparently, artists – for the inelegant act of absorbing a few dollars from a Spotify market cap built entirely on their labor.”

Anyway, the underlying question is pertinent: How much will artists actually get from UMG’s Spotify stake sale?

UMG declined to provide any hard numbers on the topic, though CFO Matt Ellis confirmed the payouts would be “consistent with our royalty policies”.

Recent history helps us make an educated guess.

As you’ll know, last month Bill Ackman launched a takeover bid for UMG that proposed raising funds by selling UMG’s full Spotify stake.

In a letter to UMG’s board, Ackman suggested that UMG’s Spotify holding (as of April 6) would generate a gross windfall of around USD $3.1 billion. From this, he said, UMG would end up with just over half – USD $1.7 billion – in net proceeds “after taxes and net of the artists’ share of Spotify proceeds”.

Indeed, Ackman suggested that UMG artists would be paid approximately USD $866 million from the sale, around 28% of the gross amount.

Based on the implied math in Ackman’s proposal, if UMG now banks $1.45 billion by selling 50% of its Spotify shares, the company would end up with approximately $805 million, with a further $240 million for the taxman.

That would leave roughly $405 million for artists, likely subdivided by each act’s Spotify ‘stream share’ for UMG over the past 18 years.

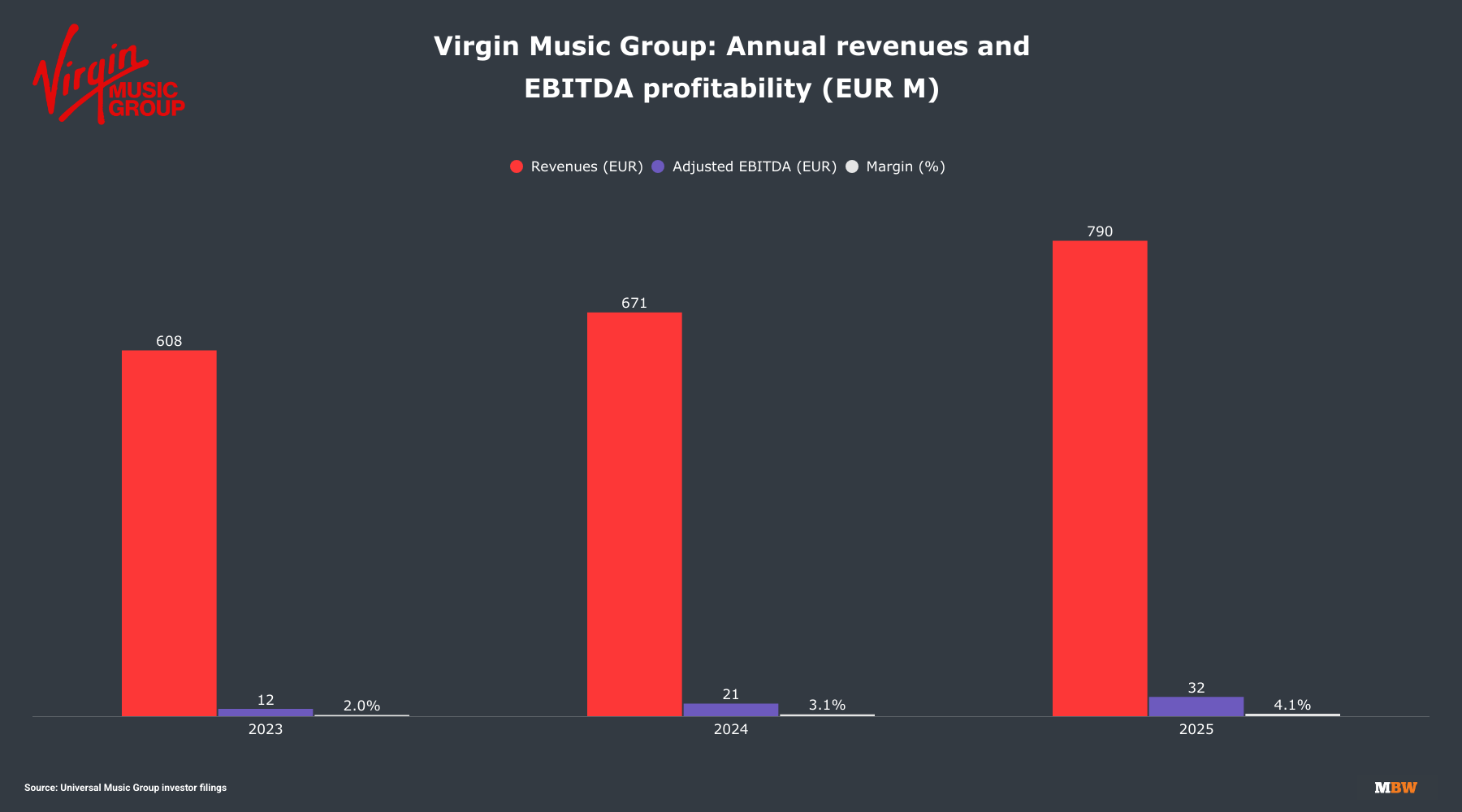

2) Thanks to UMG’s new levels of investor transparency, we have revenue numbers for Virgin Music Group. Its growth is impressive – but not all analysts will love it.

In 2022, Universal Music Group announced a major strategic pivot.

The company confirmed that it had poached mtheory founders, Nat Pastor and JT Myers, to run Virgin Music Group – a fully-fledged global indie label services division.

Speaking to analysts on UMG’s Q1 earnings call, Sir Lucian Grainge referenced this move, noting: “About 5 years ago, we foresaw a potential gap in our portfolio, something I couldn’t allow.”

VMG was launched to duke it out with Sony‘s The Orchard, which had risen into a seemingly unassailable lead as the world’s No.1 services provider to the independent sector.

Since then, of course, Universal has doubled down on its indie services business via this year’s $775 million acquisition of Downtown.

“From 2023 to 2025, VMG enjoyed a 30% rise in annual revenues, reaching EUR €790M (around USD $888M) last year. In the same timeframe, VMG also posted an improvement in bottom-line EBITDA margin.”

In an effort to increase transparency for investors, UMG broke out VMG’s standalone annual revenues for the first time in its Q1 earnings.

These figures show that, from 2023 to 2025, VMG enjoyed a 30% rise in annual revenues, reaching EUR €790M (around USD $888M) last year. In the same timeframe, VMG also posted an improvement in bottom-line EBITDA margin.

In addition to VMG’s numbers, UMG separately used its Q1 earnings to break out Downtown‘s performance since the acquisition closed on February 20 (to the end of March, 2026).

Downtown’s recorded music revenues in this 39-day period hit EUR €72M (around USD $84M), with music publishing revenues of €14M ($16M), and an EBITDA profit margin of 3.5%.

When Downtown is combined with Virgin, claimed Grainge, “we’ve leapfrogged our competitors to become the No.2 company in the fast-growing artist and label services market”.

Despite all this good news, the subject of Virgin and Downtown has mixed fortunes for UMG’s investor messaging – because the profit levels of indie services businesses typically can’t match the higher-margin performance of UMG’s frontline record companies.

What’s more, because the indie services sector is growing at a stunning pace, the lower-margin indie services divisions keep making up an increasing proportion of UMG’s total revenues.

On the Q1 call, UMG CFO Matt Ellis explained that, in 2025, Virgin contributed 8.4% of Universal’s total recorded music revenues – up from 7.5% in 2024. This, he said, “offset 20 basis points of year-over-year margin expansion” in UMG’s non-Virgin recorded music division.

In other words, as Virgin and Downtown continue to grow, they pose a challenge to UMG’s ability to increase its margins within the “mix” of its overall business.

Sir Lucian Grainge has a very clear view on this: Universal won’t be opting out of the super-fast-growing indie distribution sector in order to cosmetically boost short-term profit margins.

“Our Virgin and Downtown businesses are highly complementary, growing quickly and on a path to market leadership in a growing sector,” said Grainge. “The next phase of our plan for Virgin is focused on empowering independent players, raising the standards of service even higher, and growing our community of dynamic labels and entrepreneurs.

“At the same time, we see a meaningful opportunity for [Virgin] to capture additional value in high-potential markets.”

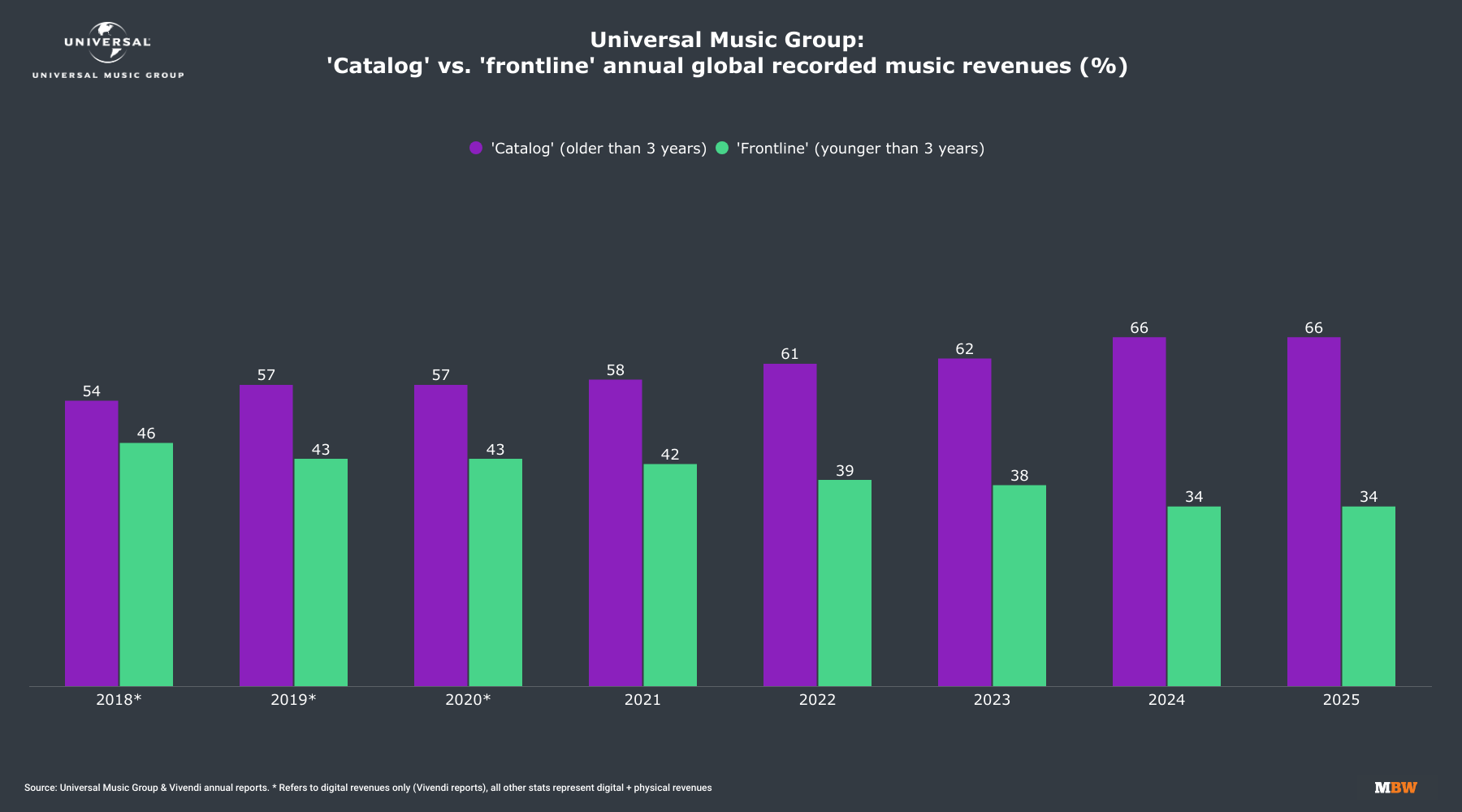

3) ‘Frontline’ and ‘catalog’ are ‘old-fashioned terms’

Back in March, on UMG’s previous quarterly earnings call (Q4 2025), the firm’s CFO Matt Ellis made a disclosure that I don’t think received nearly enough attention.

Speaking about the pricey economics of re-signing established artists, Ellis explained that royalty advances are “normally recouped not just through the future releases from our artists, but also the catalog of the prior work that audiences continue to engage with.”

i.e., When UMG pays a big advance to re-sign a superstar, it doesn’t need the next album to be a smash to get its money back. It can recoup against the artist’s entire back catalog – every stream of every old hit, compounding quietly in the background.

This matters because some of UMG’s investors are looking at the company’s catalog vs. front-line revenue split and asking: why bother with the expensive part?

In 2018, catalog accounted for 54% of UMG’s recorded music revenues. By 2025, that figure had risen to 66%.

It’s an industry-wide trend: Luminate data shows US streams of ‘current’ music actually declined in volume in 2025 YoY, with all the market growth driven by older music.

To a certain type of investor, this picture screams: Ditch the messy, expensive business of signing artists. Strip out the catalog. Enjoy higher margins.

On UMG’s Q1 call last week, BofA’s Adrien de Saint Hilaire (Mr. Leakage) prodded at this ideology by asking whether UMG could “pivot towards being more of a catalog-only business.”

The answer, emphatically, was no.

Grainge left no room for ambiguity. He called frontline and catalog “old-fashioned terms” — and said UMG views them “not as separate entities, but as one holistic opportunity.”

Then he offered proof.

On April 11, Justin Bieber headlined Coachella. During his set, he pulled out a laptop and scrolled through YouTube, singing along to old videos of himself — including the 14-year-old hit, Beauty and a Beat.

Within days, the song had surged to No.1 on Spotify and Apple Music globally, as Bieber’s average daily global streams, said Grainge, nearly quadrupled — from 31 million to 113 million.

“That’s why we don’t view ‘frontline’ and ‘catalog’ as separate entities,” said Grainge, “but as one holistic opportunity.”

To UMG, the Bieber example illustrates its model in real time.

That 66-catalog/34-frontline split isn’t two dueling businesses duct-taped together. It’s one intrinsically fused economic machine.Music Business Worldwide

{kind=link}